Biodiversity

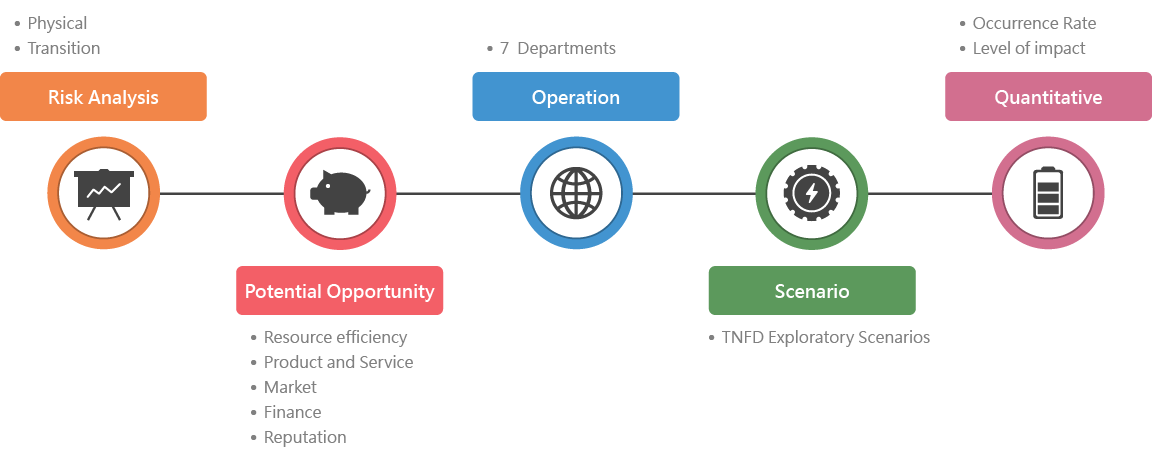

CSC adopted the LEAP (Locate, Evaluate, Assess, Prepare) framework recommended by the Taskforce on Nature-related Financial Disclosures (TNFD) as its core methodology for assessing nature-related risks.

Using the LEAP approach, CSC identified dependencies and impacts between its operational activities and key natural resources such as water, biodiversity, air quality, and soil. Based on this evaluation, significant risks and opportunities were identified to support the development of relevant management strategies and sustainability disclosures.

CSC followed the Additional Sector Guidance – Metals and Mining issued by TNFD to examine the relationship between the steel industry value chain and biodiversity. Using a location-specific approach, CSC identified priority areas that pose potential impacts on or dependencies on nature. Based on these findings, CSC conducted a further assessment of nature-related risks and opportunities, and developed targeted response strategies and performance indicators for the material topics identified.

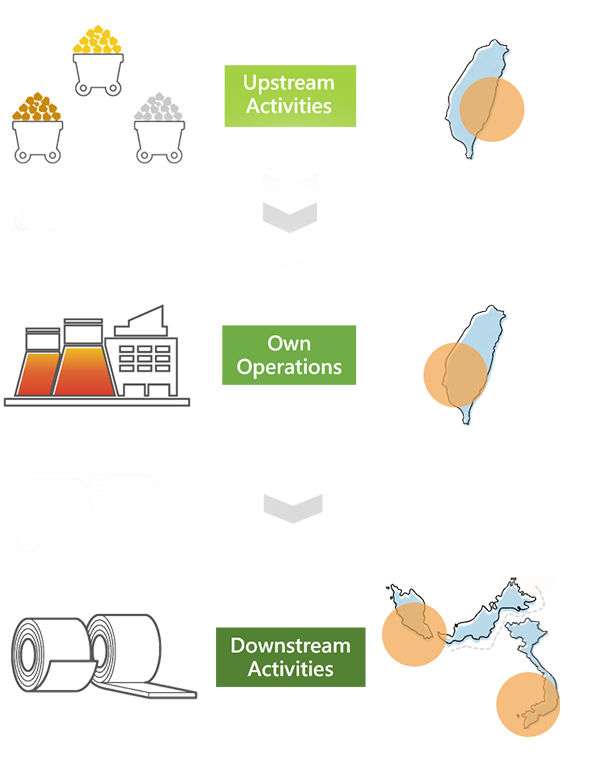

Scope of Identification

CSC Hualien Stone Handling Site(Stone Collection and Supply)

- An important base for stone collection and supply, responsible for the processing and transportation of raw materials such as limestone

CSC Head Office(Production base)

China Steel Building(Administrative Center)

Kaohsiung Park(Adjacent areas to own operations)

- CSC head office covers ironmaking, steelmaking, hot rolling, cold rolling and other processes, which are highly energy and water intensive.

- China Steel Building Manage corporate governance structure and operating policies

- The CSC Group Education Foundation adopted and maintained the Kaohsiung Park within a 2 km area around the CSC head office, providing a place for the company to practice community ecological care

CSC Steel Sdn. Bhd. CSVC(Processing and sales bases)

- Steel processing and sales base of CSC's investment in overseas. Satisfy global steel market demand through product exports, and undertake upstream materials for reprocessing and application, further extending product life cycle

Identification Results

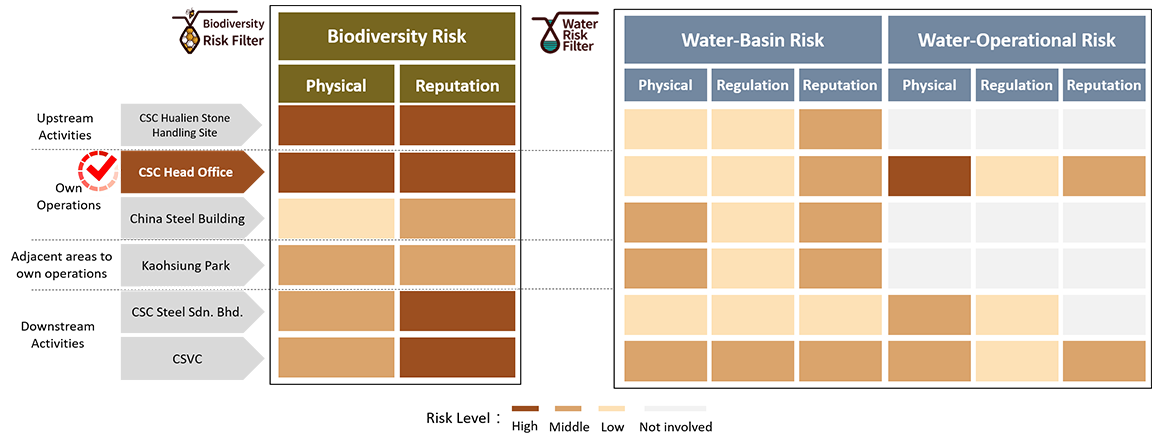

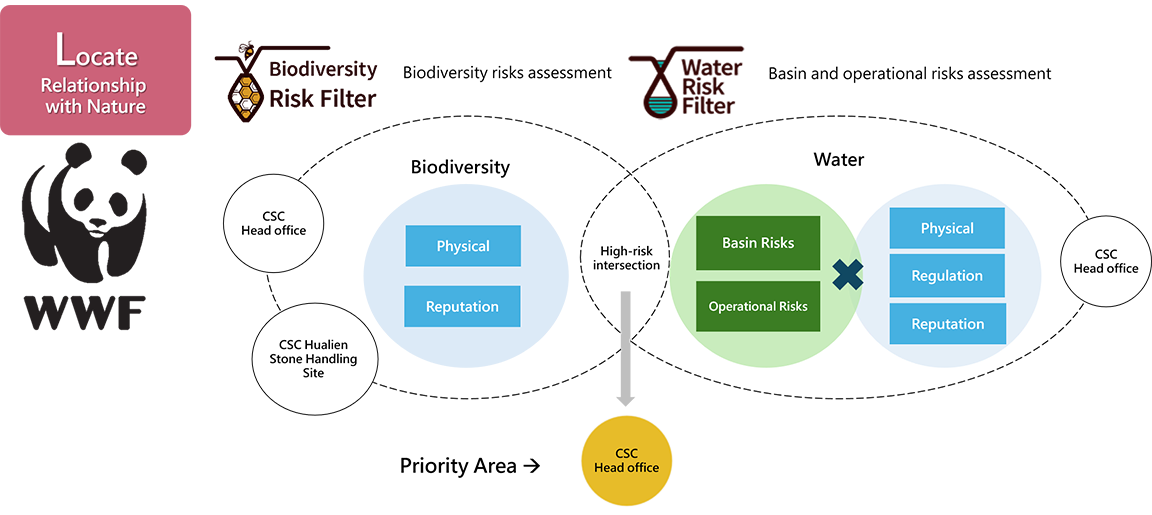

CSC applied the WWF Biodiversity Risk Filter and the WWF Water Risk Filter to analyze the risk of the value chain. Based on the cross-comparison of risk results, those locations that fall into the high-risk range of both biodiversity risk and water risk are identified as priority areas.

The Head Office and Hualien Stone Handling Site are identified as priority areas based on the result of biodiversity risk assessment, while the head office is identified as a priority area based on the result of water risk assessment. Therefore, CSC combined the cross-comparison results and decided to select the head office as the priority area.

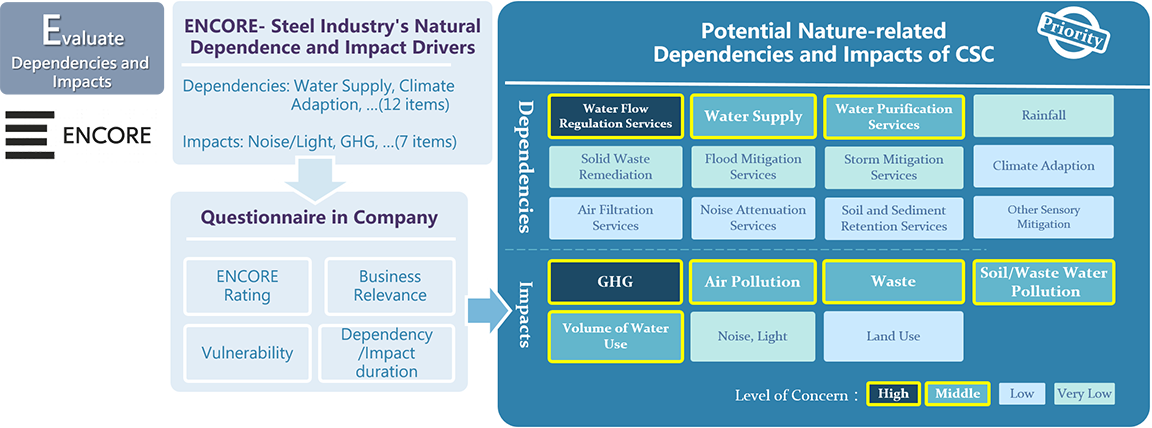

Based on the ENCORE framework, CSC identified the primary nature-related dependencies and impact drivers relevant to the steel industry, with the Head Office selected as the priority site for evaluation. A questionnaire survey was then conducted, inviting members of the TNFD task force to assess each driver in terms of business relevance, vulnerability, dependency, and duration of impact.

Scenario Analysis

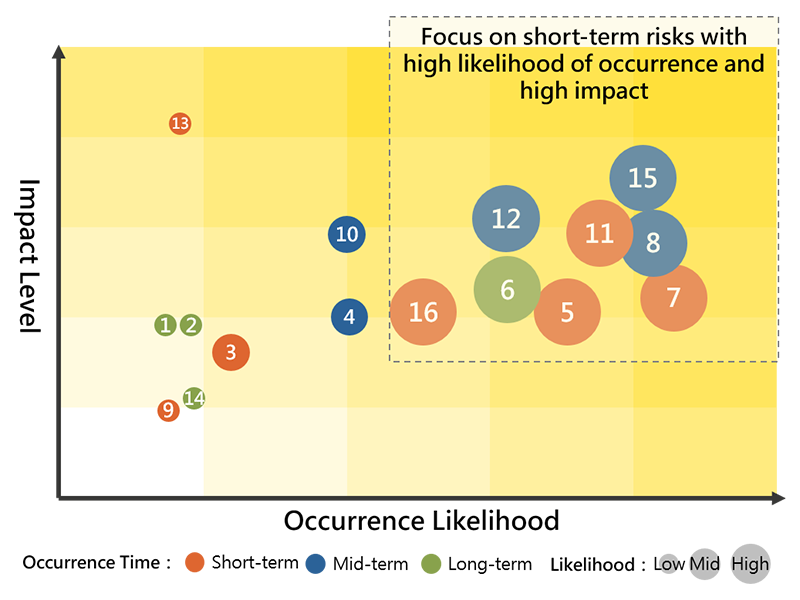

CSC used the Guidance on Scenario Analysis published by TNFD to explore the physical risks and transition risks under four scenarios. We invited managers from relevant departments to discuss the company's future strategy direction after analyzing the risks, probability of occurrence and impact of the current operating profile. A total of 16 corresponding material nature-related risks were identified based on the issues that are most relevant to CSC's business operations and the evolving scenarios of nature-related risks.

Identification of Material Nature-related Risks

Based on the results of the scenario analysis, CSC identified the significance of 16 risk topics. Among them, the material risk topics include green finance transformation, international sustainability trends, nature-related laws and policies, regulatory uncertainty, international carbon reduction trends and pressures, and reputational risks.

| Green Finance Transformation, Internal Sustainability Trends | |

|---|---|

| 1 | Sustainability taxonomy and regulations about disclosure requirement increase operational reputation risks |

| 12 | Banks/insurance companies are oriented towards green financing, increase operational financial uncertainty |

| Uncertainty in Nature-related Laws and Policies | |

| 2 | Financial impact of increasing recycled water usage |

| 3 | Financial impact of stricter environmental regulations and natural disclosure |

| 4 | Fluctuations in material costs due to changes in environmental trends |

| 5 | The transition period for sustainable information disclosure may lead to increased short-term operating costs |

| 6 | The lack of breakthrough technologies and unclear energy strategies have led to difficulties in transformation of enterprises in terms of technology and capital investment. |

| 11 | Uncertainty about green markets and energy strategies |

| 16 | Stricter environmental regulations affect operating costs |

| International Carbon Reduction Trends and Pressures | |

| 7 | Carbon reduction pressure increases demand for low-carbon raw materials, increasing raw material and R&D costs |

| 8 | Investment in new technology increases operating costs |

| 13 | The imposition of carbon fees and the potential for policy changes will lead to increased operating costs, uncertainty, and financial planning risks. |

| Dependency and Impact of Natural Resources | |

| 9 | Financial impact of extreme natural disasters |

| 14 | Risk of production outages or disruptions due to water shortages |

| 10 | Risk of monitor and reduce the hazardous substances and air pollution in the working environment |

| Reputational Risk | |

| 15 | Environmental pollution or false news triggers public opinion and affects corporate reputation |

Identification of Material Nature-related Opportunities

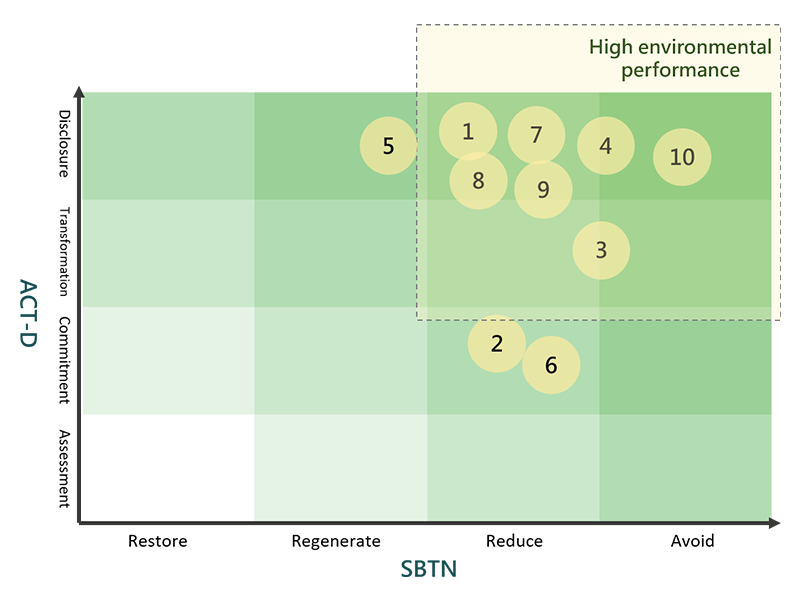

CSC adopted the SBTN action framework, systematically identifying and responding to natural impacts through the four major actions of “Avoid, Reduce, Regenerate, and Restore". At the same time, CSC used the four steps of ACT-D (Assessment, Transformation, Commitment, and Disclosure) to review the implementation of nature-related opportunities and gradually build internal management and disclosure mechanisms. Through science-based strategic actions and risk scenario analysis, CSC strengthens our resilience to natural risks and actively deploys emerging market opportunities under the green transformation.

| Issues | |

|---|---|

| 1 | The Potential of Green Steel Market |

| 2 | Ecological Investigation for Plant Areas |

| 3 | Greening Maintenance and Disaster Prevention |

| 4 | Investment on Renewable Energy |

| 5 | Green Financial and ESG |

| 6 | New Material R&D and Adaption |

| 7 | Waste Recycling |

| 8 | AI Environmental Monitoring |

| 9 | Water Recycling Management |

| 10 | Campus Environmental Education |

Biodiversity Mitigating Actions

To reduce the dependencies and impacts on biodiversity, the following mitigating measures and action plans have been implemented:

| Mitigating Measures | CSC Actions |

|---|---|

| Avoid |

|

| Reduce |

|

| Regenerate |

|

| Restore |

|

| Transform |

|

Mid- and High-Level Biodiversity Dependencies and Impacts for CSC

| Dependencies | Impacts | CSC Mitigating Actions | ||||||

|---|---|---|---|---|---|---|---|---|

| Water Flow Regulation Services | Water Supply | Water Purification Services | GHG | Air Pollution | Waste | Soil/Waste Water Pollution | Volume of Water Use | |

| V | V | For more details: Scrap Recycling (Product Certification) | ||||||

| V | V | V | For more details: Hazardous Substance Management of Products | |||||

| V | V | V | V | For more details: Water Efficiency Management Programs | ||||

| V | V | For more details: | ||||||